The commercial real estate crisis is looming on the horizon, raising concerns among financial experts about its potential economic impact. With office vacancy rates soaring in major cities and a significant portion of commercial real estate loans set to mature, many are worried that widespread bank failures could follow. This scenario is exacerbated by the Federal Reserve’s reluctance to lower interest rates, which may lead to increased delinquencies on these loans. The fallout from this crisis could ripple through the economy, affecting not only major banks but also regional lenders heavily invested in real estate. As we delve deeper into this situation, it becomes clear that understanding these connections is crucial for navigating the financial landscape in the coming years.

As we explore the evolving landscape of commercial property investments, it’s essential to recognize the challenges facing this sector. Terms like the office space downturn and real estate loan maturities highlight a troubling trend that could affect not only banks but also broader economic stability. The surge in unoccupied office buildings, coupled with concerns over rising interest rates, poses a significant dilemma for landlords and financial institutions alike. With many companies adjusting their workspace needs post-pandemic, the demand for office environments has markedly shifted, leaving a considerable number of properties at risk of devaluation. By examining these underlying factors, we can better comprehend the potential repercussions of a commercial property market under strain.

The Economic Implications of High Office Vacancy Rates

High office vacancy rates in major U.S. cities have raised alarms among economists who warn of potential broader economic repercussions. As businesses adapt to new work arrangements with many opting for remote or hybrid models, demand for office space has plummeted. Currently, vacancy rates range from 12% to 23%, which severely suppresses property values and affects revenue streams for property owners. This situation creates a critical challenge as a significant portion of commercial real estate loans comes due in the next few years, further exacerbating financial stress in this sector.

The fallout from high vacancy rates can ripple through various sectors of the economy. When businesses struggle to fill their office spaces, they may reduce spending on maintenance, renovations, or local services, leading to job losses and decreased economic activity in surrounding areas. Additionally, prolonged high vacancy levels can lead to decreased property tax revenues for municipalities, impacting public services and infrastructure spending. Therefore, understanding the economic implications of these high vacancy rates is essential for policymakers and stakeholders across the board.

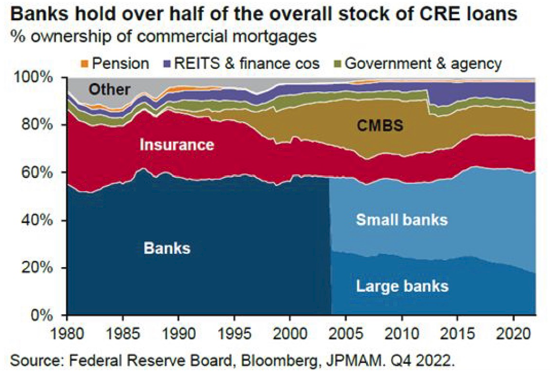

Analyzing the Commercial Real Estate Crisis

The looming commercial real estate crisis stems from several interconnected factors, including the rising numbers of delinquent loans and the uncertainty of high-interest rates. Kenneth Rogoff, a notable economist, points out that many investors over-leveraged their holdings during a period of low interest, not anticipating the impact of rising rates. This situation has left many commercial properties struggling to attract tenants, leading to a wave of potential bankruptcies as businesses adjust to the shift in working trends post-pandemic.

The consequences of the commercial real estate crisis extend beyond just property owners. Banks that invested heavily in these loans are susceptible to significant losses, which may create conditions ripe for bank failures, particularly among smaller institutions less regulated than their larger counterparts. If a cascade of defaults occurs within regional banks, the ripple effect can severely hamper credit availability and economic growth, heightening concerns about the overall stability of the financial system.

The Impact of Rising Interest Rates on Real Estate

Rising interest rates have made borrowing more expensive, leading to increased anxiety among real estate investors and lenders. As rates continue to climb, many commercial real estate loans, which were secured at lower interest rates, become less manageable, leading to a potential increase in defaults. This creates a trickle-down effect, where banks may tighten their lending practices, further stifling investment in the sector and potentially leading to broader economic slowdowns.

Moreover, the market’s reaction to rising rates is concerning. Investors may start to pull back from financing new projects or procuring real estate properties altogether, which could result in reduced economic activity in related sectors such as construction and development. Ultimately, the interaction between interest rates and commercial real estate performance may significantly influence the stability of the overall economy, making it crucial for policymakers to monitor these trends closely.

The Role of Bank Failures in the Real Estate Landscape

Bank failures, particularly among smaller institutions, could pose serious threats to the commercial real estate landscape. As these banks are heavily invested in real estate loans, significant losses could result in diminished confidence in lending practices, leading to a tightening of credit across the market. While larger institutions may remain insulated due to more stringent regulations and diversified portfolios, the interconnectivity of the banking system means that problems in the smaller banks could quickly escalate to larger concerns.

Furthermore, the repercussions of bank failures extend beyond just the financial sector; they can have real impacts on consumers and businesses reliant on credit. For example, regions with a higher concentration of small banks that invest in real estate may experience diminished lending availability, resulting in reduced consumer spending and investment. This situation underscores the importance of addressing the vulnerabilities present within the commercial real estate financing system to avert potential crises.

Economic Growth and the Commercial Real Estate Sector

The interaction between economic growth and the health of the commercial real estate sector is complex. Economists are observing how issues related to high vacancy rates and declining property values could alter investment behaviors and overall economic performance. In the broader economic landscape, while the commercial real estate sector faces significant challenges, the U.S. economy has shown resilience through a solid job market and rising stock indexes, suggesting that not all sectors are equally affected.

Nonetheless, if commercial real estate issues are not addressed, they could stall economic growth and lead to a prolonged recovery phase. Additionally, as banks begin exercising caution due to rising delinquency rates, the resulting credit crunch could create a downward pressure that stifles innovation and business expansion in other sectors of the economy. Therefore, it is vital for stakeholders to recognize and address the systemic risks posed by the commercial real estate landscape.

Mitigating the Commercial Real Estate Crisis

Mitigating the potential fallout from the commercial real estate crisis involves several strategies, including financial interventions and policy shifts. For instance, efforts from government bodies to lower interest rates or provide relief for distressed loans could help stabilize the market. Such measures could encourage refinancing and give cash-strapped businesses the breathing space they need to recover, preventing a wave of bankruptcies and foreclosures that could jeopardize lenders.

Additionally, regulatory frameworks must be evaluated to ensure that banks can manage their real estate exposures without excessive risk. This involves revisiting capital requirements and introducing stress tests specifically tailored to assess banks’ resilience against sharp declines in real estate values. By implementing these strategies, the potential for a commercial real estate crisis to undermine broader economic performance can be significantly reduced.

Consumer Consequences in a Challenging Real Estate Market

Consumers may experience various consequences stemming from a challenging commercial real estate market. With recent warnings of potential bank failures and reduced commercial lending, consumers could face stricter borrowing requirements, making it tougher to secure loans for homes, cars, or businesses. Moreover, significant losses sustained by banks could lead to decreased confidence in financial institutions, further shaking consumer trust in the economy.

In addition, regional economies heavily reliant on commercial real estate may encounter direct impacts from decreasing property values, which can lead to higher costs of goods and service shortages. Consequently, this could generate a ripple effect throughout the broader economy as consumer spending dampens, reflecting the intricate relationship between commercial real estate health and the overall financial landscape.

Potential Solutions for Office Vacancy Rates

Addressing the high office vacancy rates calls for innovative solutions that can adapt to the changing demands of the workforce. One approach could be transforming vacant office spaces into mixed-use developments that offer residential, retail, and community services. This can maximize the utility of under-utilized properties while catering to the evolving lifestyles of urban dwellers who may prefer walkable neighborhoods with a mix of live-work-play environments.

Another avenue to explore could be enhancing the attractiveness of office spaces through amenities that cater to modern work styles, such as collaborative areas, better air quality systems, and hybrid meeting capabilities. By investing in these upgrades, building owners can potentially draw more tenants back into the fold, boosting occupancy rates and re-establishing commercial viability within the real estate market.

The Need for Comprehensive Real Estate Policies

The need for comprehensive real estate policies is paramount as the market navigates through current challenges. Tailored policies addressing zoning laws, building codes, and financial assistance programs can promote a healthier balance between commercial and residential real estate. Such comprehensive policies could incentivize conversions of disused commercial spaces into residential units, thereby easing housing shortages while addressing office vacancy issues simultaneously.

Additionally, collaboration between public and private sectors is vital to drive forward-thinking solutions that can rejuvenate struggling areas. By pooling resources and expertise, stakeholders can create frameworks that prioritize sustainable development and economic recovery, thus ensuring that the adverse impacts of a commercial real estate crisis are mitigated.

Frequently Asked Questions

How are high office vacancy rates contributing to the commercial real estate crisis in 2024?

High office vacancy rates, which range from 12% to 23% in major cities like Boston, are significantly impacting the commercial real estate crisis by depressing property values and contributing to financial instability for investors and banks. As demand for office space has decreased due to the shift towards remote work, many commercial properties are becoming over-leveraged, leading to potential defaults on loans and a domino effect in the banking sector.

What is the economic impact of the commercial real estate crisis on local banks and communities?

The commercial real estate crisis is likely to have a profound economic impact on local banks, particularly smaller regional banks heavily invested in real estate loans. Increased defaults could lead to stricter lending standards and reduced consumer spending within those communities, thereby amplifying economic challenges, especially for those reliant on regional banks for financing.

Will rising interest rates worsen the commercial real estate crisis?

Yes, rising interest rates could exacerbate the commercial real estate crisis by increasing borrowing costs for investors and making it harder to refinance existing loans. This situation could lead to higher vacancy rates and more losses in property values, creating a cycle of financial distress for both borrowers and lenders.

Are bank failures a possible outcome of the current commercial real estate crisis?

While widespread bank failures are not expected, the current commercial real estate crisis could lead to the collapse of smaller financial institutions that are less regulated and more exposed to real estate loans. Larger banks are better positioned to withstand these pressures due to stricter regulations imposed after the 2008 crisis.

What sectors of commercial real estate are still performing well despite the crisis?

Certain sectors, such as high-quality, super-premium office spaces that offer amenities like advanced air filtration systems, are still performing relatively well. Additionally, niche markets and properties that cater to specific needs may continue to attract investment, distinguishing them from the broader commercial real estate crisis.

How could the commercial real estate crisis affect consumer consumers’ finances?

The commercial real estate crisis could lead to indirect impacts on consumers, particularly through potential declines in pension funds or regional banks that affect personal lending options. Consumers may face stricter credit terms or reduced access to loans, which can hinder personal financial growth and spending.

What steps can be taken to mitigate the effects of the commercial real estate crisis?

To mitigate the effects of the commercial real estate crisis, it is essential to encourage refinancing options, potentially through governmental or institutional support to stabilize low-performing assets. However, inherent challenges like zoning laws and conversion difficulties for existing properties need to be addressed as part of a comprehensive approach.

What is the outlook for the commercial real estate market beyond 2024?

The outlook for the commercial real estate market beyond 2024 remains uncertain, with potential for stabilization if interest rates soften or demand for certain types of properties increase. However, the current landscape suggests ongoing challenges as many loans mature and investors navigate a shifting economic environment, highlighting ongoing risks to banks and investors.

| Key Point | Details |

|---|---|

| High Office Vacancy Rates | Vacancy rates range from 12% to 23% in major U.S. cities, negatively impacting property values. |

| Commercial Mortgage Debt Due | 20% of $4.7 trillion commercial mortgage debt is due this year, raising concerns for banks. |

| Potential Bank Failures | Some bank failures possible, especially among small and medium-sized banks. |

| Economic Impact | Regional banks may suffer losses affecting local economies, but overall economy remains solid due to strong job and stock markets. |

| Long-term Interest Rates | High long-term interest rates hinder refinancing opportunities, causing potential losses in real estate. |

| Consumer Harm | Losses in commercial real estate could indirectly affect consumers through regional bank impacts. |

Summary

The commercial real estate crisis is characterized by high vacancy rates in office buildings and significant amounts of commercial mortgage debt coming due. Economic experts warn that while some regional banks face potential problems, a complete financial collapse is unlikely due to a solid overall economy and the strict regulations in place since 2008. The sector’s downturn, primarily caused by changes in workplace demands post-pandemic and rising interest rates, could have ripple effects in local economies, but the broader financial system is expected to remain stable.