Corporate tax rates have become a contentious issue as policymakers grapple with the legacy of the 2017 Tax Cuts and Jobs Act (TCJA). The TCJA markedly reduced the federal corporate tax rate from 35% to 21%, igniting debates over its long-term effects on the economy. As we approach 2025, when several tax provisions are set to expire, both parties are positioning themselves for a major tax overhaul. Analysis from economists like Gabriel Chodorow-Reich highlights that while reduced corporate tax rates were intended to stimulate growth, the actual impact has been mixed, with a significant drop in tax revenues. As discussions unfold, the TCJA’s influence on corporate tax rate changes and the broader economic landscape will look to shape the future of U.S. corporate taxation and fiscal policy.

The discussion around corporate taxation has intensified as the expiration of certain provisions from the Tax Cuts and Jobs Act looms on the horizon. This legislation, which fundamentally altered the landscape of American corporate taxes, aimed to invigorate the economy by lowering tax burdens on businesses. The ongoing child tax credit debate reflects broader questions about how tax structures can support households while also addressing corporate fiscal responsibilities. With a thorough analysis of U.S. corporate taxation emerging in academic circles, experts like Chodorow-Reich are dissecting the TCJA’s impact on investments and revenue. The conversation about raising or maintaining corporate tax rates is not merely a matter of finance; it hints at deeper ideological divides on economic growth and equity.

The Impact of Corporate Tax Rates on Economic Growth

The debate surrounding corporate tax rates has resurfaced with fervor as economic conditions fluctuate. Following the enactment of the Tax Cuts and Jobs Act (TCJA) in 2017, which significantly lowered corporate tax rates from 35% to 21%, there were mixed predictions about its impact on the economy. Proponents argued that reduced tax burdens would encourage corporations to reinvest in the economy, leading to job creation and wage growth. Conversely, critics, including economists like Gabriel Chodorow-Reich, have pointed out that while there was a modest uptick in business investments, the overall increase in wages fell well short of expectations. Understanding these dynamics is crucial as Congress approaches potential reforms in 2025 with these tax cuts set to expire.

In assessing the implications of corporate tax rate changes, it’s essential to consider the evidence from the TCJA. The analysis published in the Journal of Economic Perspectives revealed that while capital investments rose by approximately 11%, it came with a hefty cost to federal revenues—estimated to diminish corporate tax revenue by up to $150 billion annually. The rising corporations’ profitability post-TCJA calls for scrutiny into what truly drives economic growth. As stakeholders weigh the calls to either raise or lower corporate tax rates, the challenge remains to find a balance that fosters investment while ensuring adequate revenue for public services.

The Child Tax Credit Debate: A Key Element in Tax Reform

The Child Tax Credit (CTC) has emerged as a focal point in discussions surrounding tax reform, particularly as the expiration of TCJA provisions approaches in 2025. Advocates for an expanded CTC argue that it provides essential financial support to families, stimulating consumer spending and bolstering economic stability. The enhanced child tax credit introduced by the TCJA, which temporarily increased benefits, has delightfully improved the financial situations of many households. As the 2024 elections approach, candidates from both parties are highlighting their positions on the child tax credit, with Vice President Kamala Harris advocating for its permanent enhancement to alleviate financial strains on American families.

However, the debate over the CTC has also revealed tensions between fiscal responsibility and social welfare. Critics express concern over the financial implications of a more substantial CTC, particularly amidst ongoing discussions about corporate tax rates. The possibility of increasing corporate tax rates to finance enhanced rebates raises questions about the interplay between corporate taxation and social benefits. With firms needing to adjust to changing tax landscapes, both families and companies are eager to understand how proposals will impact their financial realities moving forward.

Analyzing the Economic Outcomes of the TCJA

The implementation of the TCJA marked a significant shift in the structure of U.S. taxation, with a pronounced focus on corporate tax cuts. Gabriel Chodorow-Reich’s analysis reveals mixed outcomes, emphasizing that although corporate tax rate reductions spurred some increase in capital investment, the anticipated robust wage growth did not materialize. In fact, the expected annual wage increase for employees was estimated at a mere $750, starkly contrasting with the projections made by the Council of Economic Advisers prior to reform. This highlights the need for a more nuanced understanding of the linkage between tax policies and economic performance.

Additionally, the temporary nature of various TCJA provisions, including those tailored to encourage new investments, presents ongoing challenges for businesses and policymakers alike. As certain beneficial provisions phase out, companies must navigate a complex environment that affects operational strategies and growth potential. This unpredictability in tax regulation could impact organizational decision-making around investments, ultimately affecting long-term economic outcomes and the overall health of the U.S. economy.

Exploring the Future of U.S. Corporate Taxation

As Congress prepares for an inevitable tax reform battle in 2025, the future of U.S. corporate taxation hangs in the balance. The TCJA’s transformative corporate tax cuts have underscored the necessity for updated laws that reflect today’s global economy. Stakeholders from both sides of the political aisle are advocating for their proposals, weighing the merits of reinstating higher corporate tax rates against the potential benefits of maintaining tax cuts to spur innovation and investment.

Economists emphasize careful evaluation of prior corporate tax modifications, particularly how they interact with labor markets and overall economic health. Chodorow-Reich’s work suggests that options exist, such as raising tax rates while reinstating effective expensing measures, which may generate the revenue needed without stifling growth. As legislators outline their visions for a more equitable tax system, examining the impacts of corporate tax rate changes in relation to business strategies will be pivotal in shaping America’s fiscal future.

Lessons from the TCJA on Investment Behavior

The analysis of the TCJA shows that changes in corporate tax rates can significantly influence investment behavior, but understanding the nuances is vital. Chodorow-Reich’s research indicates that while lowering the statutory tax rates spurred a minor uptick in capital investments, the more prominent drivers of growth were provisions designed explicitly for expensing. This evidence highlights that alternates to a flat corporate tax rate might be more strategically effective in targeting investment growth where it counts most.

Looking ahead, lawmakers could harness lessons gleaned from the TCJA in crafting a framework that not only supports business investment but also addresses the concerns of constituents who may not have reaped the tangible benefits of the previous tax cuts. By focusing on targeted incentives rather than broad rate changes alone, Congress may foster a robust investment climate that adheres to economic need without neglecting fiscal responsibility.

Understanding the Revenue Implications of Corporate Tax Changes

One of the most glaring consequences of the TCJA was the immediate revenue drop experienced by the federal government, plummeting by nearly 40% post-implementation. This substantial loss necessitated a discussion around fiscal responsibility and new revenue streams. As corporate profits began to rebound following the initial drop, the debate intensified about whether the reductions in corporate tax rates ultimately stimulate or hinder federal revenue generation.

Analyzing the revenue implications of corporate tax changes is essential for future policy considerations. Researchers and analysts continue to examine the correlating factors, including shifts in corporate behavior and external global market pressures, to understand better how tax structures can both support economic growth and maintain government funding. As public understanding of these dynamics evolves, clear communication around fiscal strategies will be crucial in navigating upcoming challenges in tax policy.

Political Strategies Surrounding Corporate Taxation Debates

The dialogue surrounding corporate tax rates is charged with political implications as key stakeholders attempt to sway public opinion ahead of the 2024 elections. The approaches vary widely, with some candidates arguing for increased corporate taxes to fund social programs, while others warn that this would stifle economic growth. Chodorow-Reich’s insights shed light on how economic research can be harnessed to inform political strategies and articulate a fact-based narrative regarding tax policy impacts.

Political narratives can greatly affect the practical implementation of tax reforms. Increased scrutiny on how corporations respond to changing tax rates can shift voter sentiment and influence legislative agendas. As both parties prepare for a contentious electoral environment, understanding constituents’ minds and policies will be paramount in crafting appeals that resonate, especially amidst concerns over economic stability and fiscal responsibility.

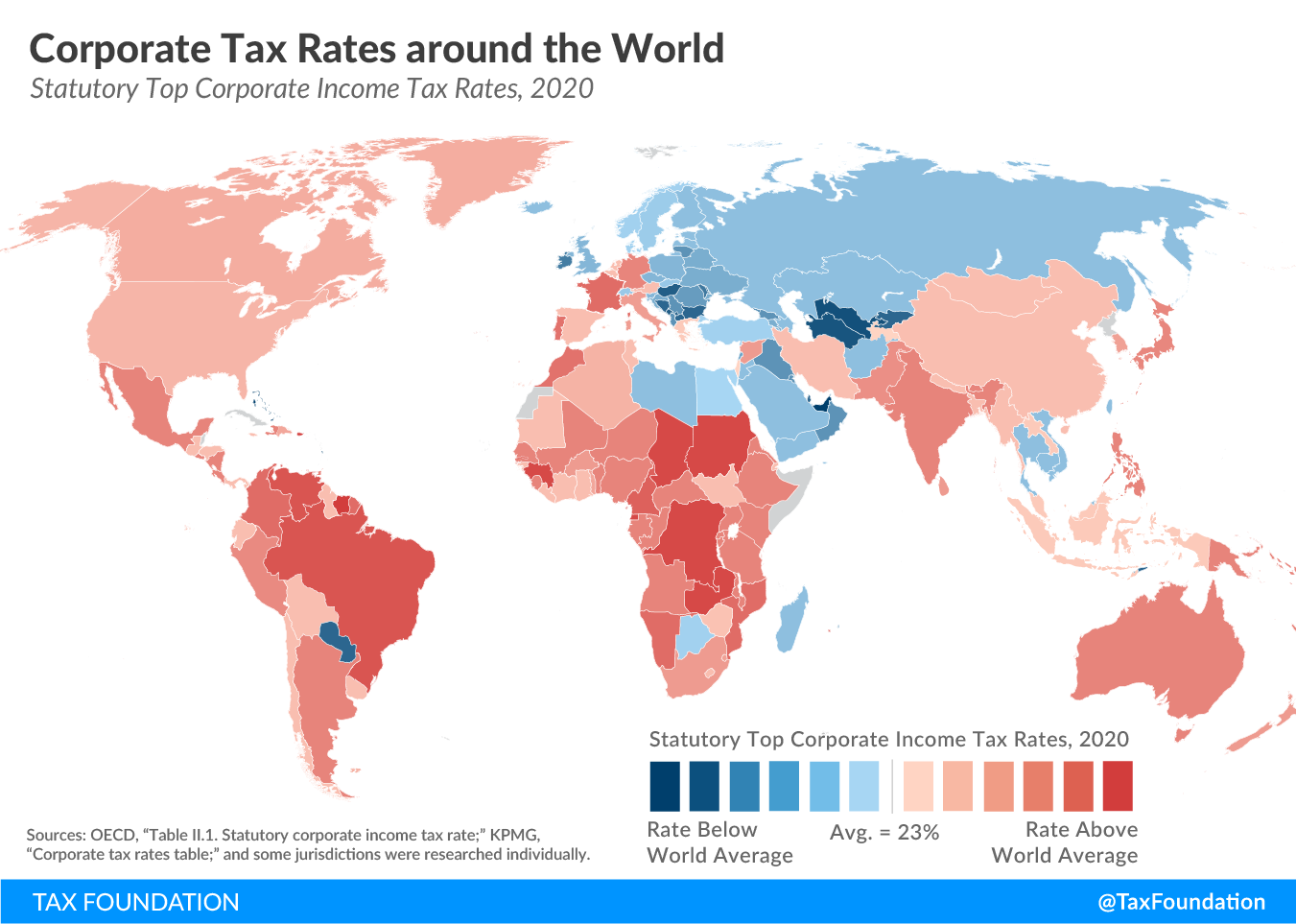

The Global Perspective on U.S. Corporate Tax Rates

The landscape of global corporate taxation has changed significantly over the past few decades, raising the stakes for U.S. corporate tax policies. With countries worldwide lowering their tax rates to attract foreign investment, the U.S. found itself competing in a dynamic international arena where high corporate rates risk driving business entities to more tax-friendly jurisdictions. The TCJA aimed to address this competitive landscape by cutting the corporate tax rate, but the ongoing debate highlights the complexities of retaining competitive edge while ensuring adequate government revenues.

Examining the international responses to U.S. corporate taxation provides critical context for future policy decisions. The interconnectedness of global markets requires that U.S. lawmakers consider not only domestic economic impacts but also international implications of tax regulations. As industries adapt to shifts in both taxation and global commerce, strategizing around corporate tax rates will be essential for attracting investment and fostering a robust economic environment.

Evaluating the Effects of Historical Corporate Tax Reforms

Historically, corporate tax reforms have oscillated between extensive cuts and substantial increases, reflecting changing economic and political priorities. By referencing past legislative actions, such as the Tax Reform Act of 1986, stakeholders can glean valuable lessons about the long-term consequences of corporate tax rate adjustments. Chodorow-Reich’s recent analyses illustrate that while immediate impacts may favor businesses, the broader economic effects require a more profound examination of how such policies affect revenue over time.

Investigating these historical contexts can inform current debates around the TCJA and other proposals aiming to modify corporate tax rates. As parties and policymakers consider which alterations will truly benefit the economy, they must look beyond short-term gains and assess how these changes ALIGN with sustainable economic growth and ample public funding. Engaging with historical data will be crucial in shaping a forward-thinking tax policy.

Frequently Asked Questions

What are the main corporate tax rate changes introduced by the Tax Cuts and Jobs Act (TCJA)?

The Tax Cuts and Jobs Act (TCJA), enacted in December 2017, permanently reduced the U.S. corporate tax rate from 35% to 21%. This significant change aimed to enhance the competitiveness of U.S. corporations in the global market by lowering the statutory tax burden, thereby encouraging business investment and economic growth.

How did the TCJA impact corporate tax revenue in the U.S.?

Following the implementation of the TCJA, federal corporate tax revenue initially dropped by approximately 40%. However, starting in 2020, corporate tax revenue began to recover as business profits exceeded expectations, partly due to the increased competitiveness afforded by the lower corporate tax rates under the TCJA.

What is the debate surrounding corporate tax rates and economic growth after the TCJA?

The debate revolves around whether the corporate tax rate cuts from the TCJA effectively stimulated economic growth. While proponents claim that lower taxes led to higher investment and wages, studies, including those from Gabriel Chodorow-Reich, indicate that the increase in wages was modest, challenging the narrative that tax cuts alone can drive significant economic benefits.

How does the TCJA impact future tax legislation focusing on corporate taxation?

The expiration of key TCJA provisions in 2025 has reignited discussions in Congress regarding corporate taxation. There is potential for adjustments in corporate tax rates and provisions, as lawmakers consider the balance between stimulating growth and addressing revenue shortfalls caused by previous tax cuts.

In what ways did corporate tax changes under the TCJA influence investment behavior?

The TCJA included provisions allowing firms to immediately deduct the full cost of new capital expenditures, which proved more effective at driving investment compared to traditional statutory rate cuts alone. This indicates that while the corporate tax rate changes lowered taxes, specific expensing measures played a critical role in incentivizing business investments.

What role does the Child Tax Credit debate play in discussions about corporate tax rates?

The Child Tax Credit debate intersects with corporate tax discussions as lawmakers evaluate revenue sources to fund various initiatives. Some Democrats propose raising corporate tax rates to support household initiatives like the Child Tax Credit, showcasing a conflict between corporate tax policy and social spending goals.

What insights did the Journal of Economic Perspectives provide on the TCJA’s long-term effects on corporate taxation?

The Journal of Economic Perspectives highlighted that while corporate tax cuts under the TCJA saw modest increases in capital investments, they also led to significant revenue declines. This suggests that while some growth occurred, the overall effectiveness of the corporate tax rate changes in stimulating sustainable economic benefits is still debated.

How have perceptions of corporate taxation shifted since the TCJA was implemented?

Since the TCJA, perceptions of corporate taxation have shifted to recognize the complexities involved. Many economists and policymakers now emphasize a balance between competitive tax rates and sufficient revenue generation to fund public services, suggesting that a one-size-fits-all approach to corporate taxation may not be effective.

| Key Points | Details |

|---|---|

| 2017 Tax Reform Dilemma | Key tax cuts and provisions under debate as the TCJA is set to expire. |

| Bipartisan Perspectives | Democrats favor higher corporate tax rates for funding; Republicans argue for further cuts to stimulate growth. |

| TCJA’s Impact on Economy | Analysis shows modest investment increase but significant revenue loss; corporate tax cuts did not pay for themselves. |

| Changes in Corporate Landscape | The US shifted from one of the lowest to a higher corporate tax rate among developed nations. |

| Future Considerations | To maintain revenue, potential for raising corporate tax rates while reinstating deductions is suggested. |

| Proposed Wage Increases | Predicted wages rose less than expected, suggesting prior projections may have been overly optimistic. |

Summary

Corporate tax rates have become a crucial topic as lawmakers approach 2025 and the expiration of the Tax Cuts and Jobs Act. The recent analysis by Gabriel Chodorow-Reich indicates that while the TCJA led to some business growth, it ultimately resulted in a significant decrease in federal tax revenue. As both parties eye future reforms, the debate surrounding corporate tax rates will undoubtedly shape economic strategies moving forward, highlighting the complexity of balancing tax policy with economic growth.